What Should My Financial Health be in my early 20s?

You’re in your 20’s. Maybe you’re in college, working a full-time job, starting a family, or still trying to figure things out. Whatever it may be, you may have wondered: “How much money should I have right now?” or “Where should I be, financially, at this point in life?” In this comprehensive guide, What Should My Financial Health be in my early 20s? we’ll try to answer these questions by exploring what financial health should look like in your early 20s. We’ll delve into topics like budgeting, saving, managing debt, and investing.

Understanding Financial Health in Your 20s

Financial health is a measure of your financial well-being. It’s about having control over your finances, being able to handle financial shocks, and being on track to meet your financial goals.

In your early 20s, you’re likely at the beginning of your financial journey. You might be dealing with student loans, starting your first job, or moving out on your own. These are all significant financial milestones that can impact your financial health.

There are several key indicators of financial health that will help you understand how you are doing. These include:

- Having a budget and sticking to it. This shows that you have control over your finances and are living within your means.

- Having an emergency fund. This is a safety net that can cover unexpected expenses, providing financial security in times of crisis.

- Managing debt, which includes making regular payments on time and keeping your debt-to-income ratio low.

- A good credit score, because it shows that you’re responsible with credit and can open doors to better financial opportunities.

Understanding these key indicators and accomplishing them will allow you to take advantage of future financial opportunities as they arise. Whether it’s buying a home, starting a business, or pursuing further education, good financial health can make these goals attainable.

Let’s dive more into these indicators and how you can accomplish them!

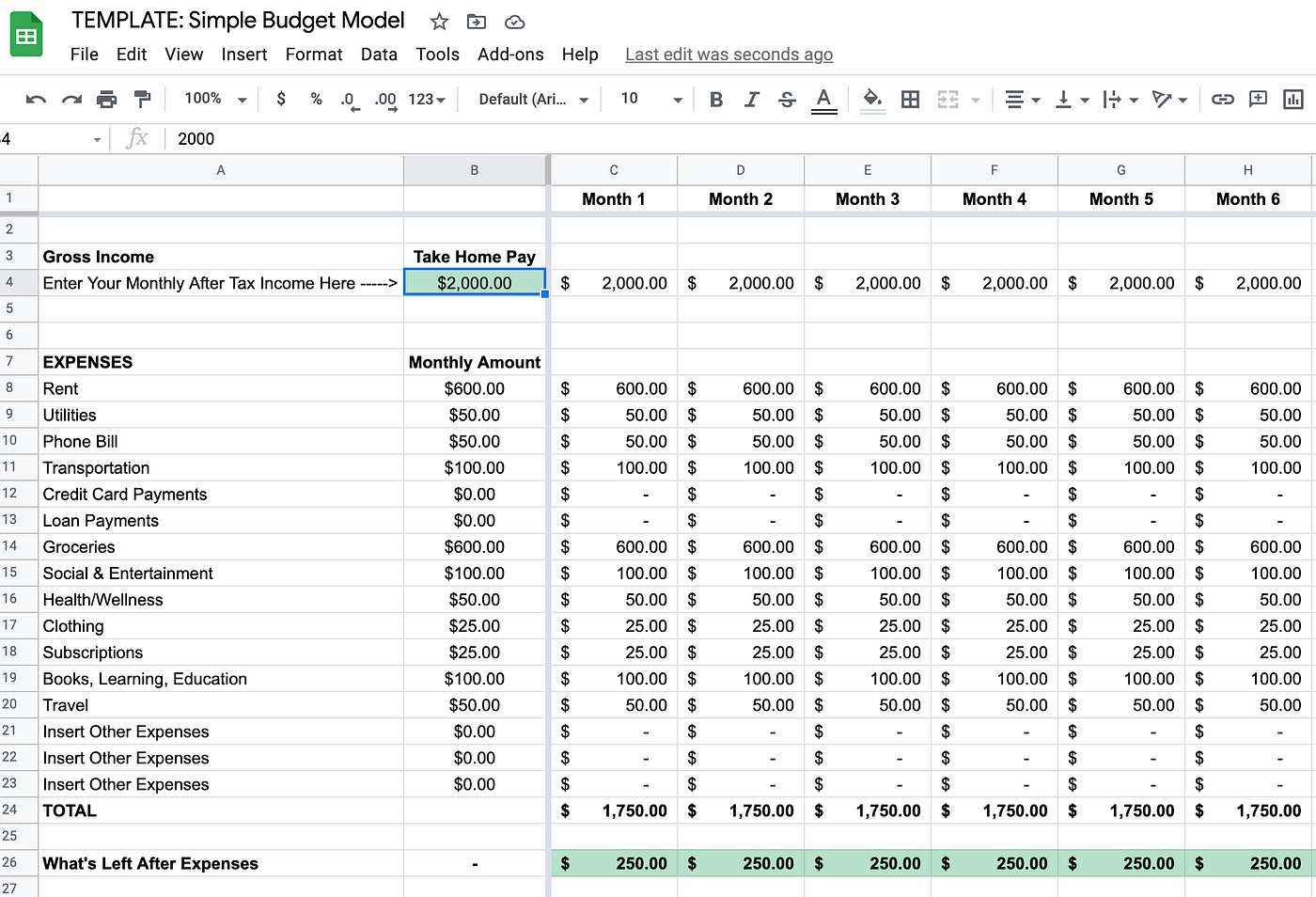

Budgeting: Your Financial Blueprint

Budgeting is a crucial part of maintaining financial health. It’s a plan for your money, outlining how much you expect to earn and how you plan to spend it. A well-crafted budget can help you meet your financial goals. It can guide your spending decisions, helping you prioritize needs over wants.

Moreover, a budget can provide a clear picture of your financial situation. It can highlight areas where you might be overspending and areas where you could save more.

Here are some steps to create a budget:

- Identify your income sources

- “I made $1,600 this month”

- List all your expenses

- “Rent is $500, gas is $80, take-out is $25, subscriptions are $20, etc…”

- Set financial goals

- “I want $200 leftover to save for my upcoming trip.”

- Distribute your income to your expenses and goals

- “After I subtracted all the expenses from my income, I am left with $95.”

- Monitor and adjust your budget as needed

- “I was short $105 for my saving goal, let’s spend less money on take-out and groceries next month.”

Creating a Realistic Budget

Creating a realistic budget is key to its success. It should reflect your actual income and expenses, not idealized versions of them.

Start by tracking your income and expenses for a few months. This will give you a clear picture of where your money is going.

Then, use this information to create a budget that aligns with your financial goals. Remember, your budget is a living document. It should be flexible and adaptable to changes in your financial situation.

Tools and Apps to Help with Budgeting

There are many tools and apps available to help with budgeting. These can automate the process, making it easier to track your income and expenses.

Some popular app options include Mint, YNAB (You Need A Budget), and PocketGuard. These tools can sync with your bank accounts, categorize your transactions, and provide insights into your spending habits. Or, if you are a member of UCCU, you can get access to a budgeting function on our mobile app!

You can also track your budget yourself using google sheets, microsoft excel, or other online tools.

Saving Money

Saving is another key aspect of financial health. It provides a safety net and helps you achieve your financial goals. The amount you should save depends on your income, expenses, and financial goals. However, a common rule of thumb is to save 20% of your income.

Emergency Fund

An emergency fund is a specific type of savings because it’s money set aside to cover unexpected expenses, such as car repairs or medical bills.

Here are some steps to start saving and build an emergency fund:

- Determine how much you need in your emergency fund (experts say to have enough to cover 3-6 months of living expenses)

- Set a monthly savings goal

- Automate your savings

- Keep your emergency fund in a separate, easily accessible account

Tips for Growing Your Savings

Growing your savings requires discipline and consistency. Start by setting a realistic savings goal and make regular contributions to your savings account.

Consider automating your savings. This means setting up automatic transfers from your checking account to your savings account. Automation can make saving easier and ensure that it happens regularly.

Also, a good way to set effective saving goals is to use the “SMART” acronym! This acronym stands for Specific, Measurable, Achievable, Relevant, and Time-bound.

For instance, instead of saying “I want to save money”, a SMART goal would be “I want to save $5,000 for a vacation in two years”.

Managing Debt and Credit

Managing debt and understanding credit are crucial for financial health. Debt, if not managed properly, can lead to financial stress and limit your financial opportunities.

On the other hand, credit, when used wisely, can be a powerful financial tool. It can help you make large purchases, build your credit history, and even save money through rewards and cash back.

Here are some tips for managing debt and credit:

- Pay your bills on time

- Keep your credit card balances low

- Don’t take on more debt than you can afford

- Regularly check your credit report for errors

- Use the “debt snowball” method to strategically pay off each debt

Understanding Credit Scores

Your credit score is a numerical representation of your creditworthiness. It’s based on your credit history, including your payment history, the amount of debt you have, and the length of your credit history.

A good credit score can open up financial opportunities, such as lower interest rates on loans and credit cards. Therefore, understanding and maintaining a good credit score is essential for financial health.

To learn more about credit scores, read this blog.

Investing in Your Future

Investing is a key component of financial health. It allows your money to grow over time, providing you with a larger financial cushion for the future.

Investing can seem intimidating, especially if you’re just starting out. However, with a little research and planning, you can start investing in a way that aligns with your financial goals and risk tolerance.

Here are some tips for investing:

- Start small and gradually increase your investments

- Diversify your investment portfolio

- Consider long-term investments for greater returns

- Regularly review and adjust your investment strategy

Examples of investment opportunities include stocks, bonds, mutual funds, real estate, and more. Know that each type of investment comes with its own set of risks and rewards. Therefore, it’s important to do your research and consider seeking advice from a financial advisor before making any major investment decisions.

Retirement Savings Plans: 401(k)s and IRAs

Retirement may seem far off when you’re in your 20s, but it’s never too early to start saving. In fact, the earlier you start, the more time your money has to grow.

Two common types of retirement savings accounts are 401(k)s and Individual Retirement Accounts (IRAs). Both offer tax advantages that can help your savings grow more quickly.

Insurance and Protection

Insurance is a crucial part of financial health. It provides a safety net for unexpected events that could otherwise lead to financial hardship.

There are many types of insurance, including health, auto, renters, and life insurance. Each serves a specific purpose and can protect you from different types of financial risks that could cost you a lot more than without insurance.

Choosing the right insurance policies can be challenging. It requires understanding your needs and comparing different options to find the best fit. Remember, the cheapest policy isn’t always the best. It’s important to consider the coverage, deductibles, and out-of-pocket costs when choosing an insurance policy.

Remember to do Regular Financial Check-Ups

Just like your physical health, your financial health needs regular check-ups too. These check-ups help you track your progress towards your goals and make necessary adjustments.

You can do a financial check-up bi-weekly, monthly, quarterly, or annually. During these check-ups, review your budget, savings, investments, and debts. Make sure you’re on track to meet your financial goals and adjust if you’re not!

You Can do it!

Though it can be difficult sometimes, it will pay off to achieve good financial health in your 20s. This involves making informed decisions about budgeting, saving, investing, and managing debt.

Remember, financial health is not a destination but a journey. It requires consistent effort, discipline, and adaptability. With the right knowledge and tools, you can navigate your financial journey successfully and build a secure future.

Need help? UCCU is always here to help! Explore our website or talk to an expert today to learn more about our financial tools that can help you!